Agricultural Accounting: Financial Data for Farm Businesses

Although the expense might seem high, good accountants will be able to save you money in the long run. With their understanding of tax legislation they may be able to reduce your tax bill, perhaps enough to cancel out the cost of your accountant’s bill. One year you might find there’s a big subsidy on cheese production, another year it might be beef that’s subsidized. Quite often governments get it wrong, leading to surpluses that drive down prices too far. The so-called “butter mountains” and “wine lakes” in Europe towards the end of last century were partly a result of poorly-managed subsidies.

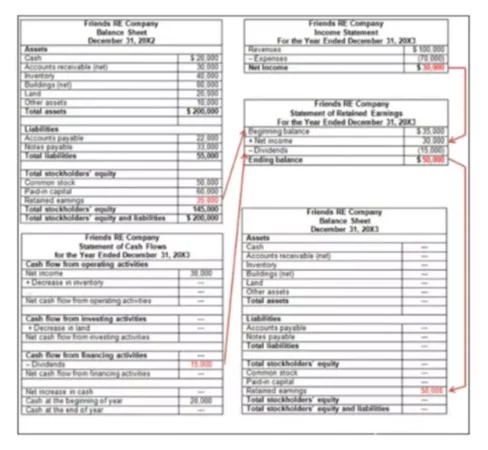

Consider hiring an accountant

With evolving regulations in the agricultural industry, compliance has become increasingly complex. Agricultural accountants ensure farms adhere to industry and regulatory standards. Moreover, biological assets, such as crops and livestock, can vary greatly in value based on growth, diseases, and market fluctuations. The importance of understanding the timing of cash flows, the cost of production, and farm profitability cannot be overstated. Agricultural accountants deal with the complex financial landscape of the farming industry. They handle daily transactions, analyze financial data, and prepare financial reports.

Technological Advancements in Accounting

This can cause long-term headaches if you’re trying to keep a tally of the animals on your farm. Today subsidies are managed more efficiently, but that can mean they change more often too. So make sure you keep track of subsidies and account for them, especially if they’re made as direct payments. The more knowledge you have about subsidies, the more you can plan your farming strategy to make the most of them.

Agricultural accounting Q&A

- Today subsidies are managed more efficiently, but that can mean they change more often too.

- Artificial intelligence (AI) and machine learning (ML) are at the forefront of this transformation.

- Or, if moving to a livestock farming model, be sure to record the cost of buying stock.

- Under accrual accounting, you generally report income in the year earned and deduct or capitalize expenses in the year incurred.

- Bearer plants would include tea bushes, grape vines and rubber trees.

- Agricultural accounting operates on a set of specialized principles designed to reflect the unique aspects of the industry.

The point of harvest represents the transition between accounting for agricultural produce assets under IAS 41 and IAS 2. Fair value less costs to sell at the point of harvest forms ‘cost’ for the purposes of IAS 2. The standard specifically requires that fair value not be determined by reference to a future sales contract. Contract prices are not necessarily relevant in determining fair value, because fair value reflects the current market in which a willing buyer and seller would enter into a transaction. As a result, the fair value of a biological asset or agricultural produce is not adjusted because of the existence of a contract. Financial reporting in agriculture is tailored to convey the sector’s unique economic activities, providing transparency and accountability.

Software solutions now enable real-time data entry and analysis, reducing the likelihood of errors and the time required for data reconciliation. Cloud-based platforms have revolutionized the way financial information is stored and accessed, allowing for secure, scalable, and collaborative environments that stakeholders can access from anywhere in the world. The IFRS Foundation is a not-for-profit, public interest organisation established to develop high-quality, understandable, enforceable and globally accepted accounting and sustainability disclosure standards. Nondeductible farm expenses include personal, living, and family expenses, such as the cost of maintaining your personal vehicles or horses. You also cannot deduct expenses such as loan repayment, loss of livestock (if you deducted the cost of raising them as an expense), or membership fees (e.g., country club).

Managing Financial Aspects in Agriculture

All of our content is based on objective analysis, and the opinions are our own. They monitor changes in laws, analyze their implications, and implement necessary adjustments to business practices. Through thorough financial analysis, they can highlight areas of the business that are underperforming and suggest corrective measures. International Accounting Standard IAS 41, Agriculture, is the first standard that specifically covers the primary sector. Learn about the eight core bookkeeping jobs, from data entry to reporting and tax prep.

Usually the simplest solution is to go with the government’s definition of significant dates and livestock ages when doing your accounts. It may not always be factually correct, but it’ll save you going through more complex calculations in the future. Master the principles of auditing, derivatives, corporate finance, and managerial and financial accounting and learn how to apply them in production, processing, or retailing sectors of the food and agriculture industry. The landscape of accounting has been reshaped by technological advancements, which have automated traditional processes and introduced new efficiencies.

Agricultural produce is measured at fair value less estimated costs to sell at the point of harvest. [IAS 41.13] Because harvested produce is a marketable commodity, there is no ‘measurement reliability’ exception for produce. Agricultural accountants serve as crucial pillars in the farming industry, navigating the complex and unique financial landscape of agribusiness. Government grants – assets measured at cost less accumulated depreciation and impairment IAS 20 will apply. The standard also addresses the situation where the biological assets are physically attached to the land eg trees in a forestry plantation.

You must file Form 943 if you paid wages subject to employment tax (federal income, Social Security, and Medicare) withholding to one or more farmworkers. Schedule J (Form 1040), Income Averaging for Farmers and Fishermen, is a form you can use to average your taxable farm income. Take self-paced courses to master the fundamentals of finance and connect with like-minded individuals. A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation. Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise.

Download our FREE whitepaper, Business Guide to Navigating Through Disasters & Emergencies, for overviews and government links.